Reining in Production - Hunkering Down as Margins, Supplies Rebalance

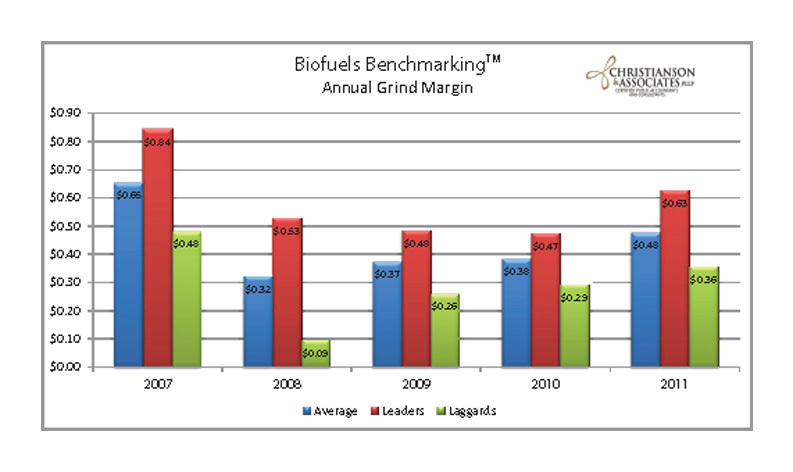

SOURCE: CHRISTIANSON & ASSOCIATES

April 11, 2012

BY Holly Jessen

Advertisement

Advertisement

Upcoming Events

Team M3 Meeting

August 10-13, 2026

SOUTH SIOUX CITY MARRIOTT RIVERFRONT | SOUTH SIOUX CITY,NEBRASKA

For nearly two decades, the TEAM M3 Meeting has served as one of the ethanol industry’s most collaborative and practical maintenance-focused gatherings. Built by maintenance managers for maintenance managers, the event creates an environment where ethanol producers, plant personnel and industry vendors openly share operational challenges, maintenance solutions and reliability strategies. The 2026 TEAM M3 Meeting is being explored as a continuation of the same peer-driven event style and Sioux City-area location the industry has supported for years — while enhancing communication, exhibitor coordination, sponsorship opportunities and overall event organization.View More

North American SAF Conference & Expo

August 25-27, 2026

GREATER TACOMA CONVENTION CENTER | TACOMA,WASHINGTON

Taking place August 25-27, 2026 in Tacoma, Washington, the North American SAF Conference & Expo, produced by SAF Magazine, in collaboration with the Commercial Aviation Alternative Fuels Initiative (CAAFI) will showcase the latest strategies for aviation fuel decarbonization, solutions for key industry challenges, and highlight the current opportunities for airlines, corporations and fuel producers. The North American SAF Conference & Expo is designed to promote the development and adoption of practical solutions to produce SAF and decarbonize the aviation sector. Exhibitors will connect with attendees and showcase the latest technologies and services currently offered within the industry. During two days of live sessions, attendees will learn from industry experts and gain knowledge to become better informed to guide business decisions as the SAF industry continues to expand. View More

2027 International Biomass Conference & Expo

March 2-4, 2027

COBB CONVENTION CENTER | ATLANTA,GEORGIA

Now in its 20th year, the International Biomass Conference & Expo is expected to bring together more than 1000 attendees, 180 exhibitors and 100 speakers from more than 25 countries. It is the largest gathering of biomass professionals and academics in the world. The conference provides relevant content and unparalleled networking opportunities in a dynamic business-to-business environment. In addition to abundant networking opportunities, the largest biomass conference in the world is renowned for its outstanding programming—powered by Biomass Magazine–that maintains a strong focus on commercial-scale biomass production, new technology, and near-term research and development. Join us at the International Biomass Conference & Expo as we enter this new and exciting era in biomass energy.View More

North American Biocarbon Conference

March 2-4, 2027

COBB CONVENTION CENTER | ATLANTA,GEORGIA

The North American Biocarbon Conference, co-located with the International Biomass Conference & Expo, brings together the full value chain of carbon-negative and carbon-smart technologies in one powerful, integrated event. By aligning biocarbon producers, biomass power generators, biochar innovators, carbon-removal buyers, project developers, and equipment providers with the broader biomass, biogas, CHP, pellet, and renewable-power industries, this co-located experience creates unmatched cross-sector engagement. Attendees gain access to expanded networking opportunities, dual-track educational programming, a unified expo hall, and a broader pool of commercial partners—all designed to accelerate the deployment of biocarbon solutions, scale climate-positive markets, and strengthen the emerging carbon-removal economy across North America.View More

International Fuel Ethanol Workshop & Expo

June 14-16, 2027

CHI HEALTH CENTER | OMAHA,NEBRASKA

Now in its 43rd year, the FEW provides the ethanol industry with cutting-edge content and unparalleled networking opportunities in a dynamic business-to-business environment. As the largest, longest running ethanol conference in the world, the FEW is renowned for its superb programming—powered by Ethanol Producer Magazine —that maintains a strong focus on commercial-scale ethanol production, new technology, and near-term research and development. The event draws more than 2,300 people from over 31 countries and from nearly every ethanol plant in the United States and Canada.View More

@ Copyright 2026 - BBI International - All rights reserved.