Siting a New Bioenergy Facility: Pitfalls and Preconditions

PHOTO: TIM PORTZ

January 10, 2020

BY Stan Parton

Part of Forest2Market’s business is tracking emerging industries that use wood raw material feedstocks. We began serving bioenergy markets in 2006, and as biofuel and biochemical markets have advanced, we added these technologies to our practice. Through our work in this sector, we have developed several unique analytical methodologies to help project developers better understand qualified feedstocks, the wood supply chain and the economic and biological sustainability of wood-derived feedstocks. We have also uncovered major project development pitfalls that could potentially consume capital and sink new projects before they even get off the ground.

Understanding the feedstock supply chain is a critical first step for biobased projects before moving to the site selection phase. At a minimum, developers must have fact-based answers to a series of critical questions:

• What are the market drivers of supply?

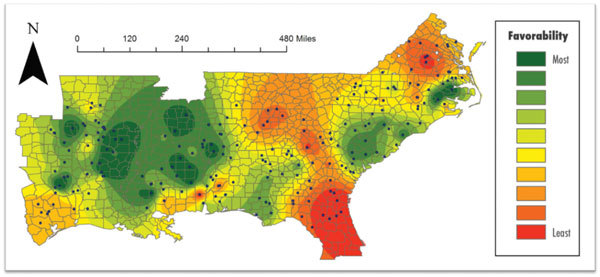

• Where should I site my plant to assure long-term sustainability?

• What is the competitive demand in the market and how easily can that demand be displaced?

• How much excess supply exists?

• How do I track sustainability?

• How do I hedge feedstock price volatility?

• How do I make my debt or equity partners comfortable with supply chain risks?

From this exercise and analysis, developers can create a list of essential criteria so that each potential project location can be thoroughly and objectively vetted and ranked. While governmental economic incentives are helpful inducements in determining prospective site locations, an approach that places these considerations ahead of objective feedstock considerations and assessment could jeopardize the success of a project in the long run.

It can be tempting to take advantage of economic incentives, but reality is that feedstock costs compose an enormous part of the overall operating cost of a facility—upward of 70 percent in many cases. Siting a new project in an optimal wood basin is therefore critical to ensuring that a sustainable and affordable wood supply is available throughout the life of the project. The following are the some of the costliest pitfalls to avoid when siting a facility.

Relying solely on local suppliers for market information. Wood markets are dictated by local supply and local demand, yet this does not position local suppliers to accurately assess the market. The view held by each local supplier is limited to the opportunities surrounding only his or her supply, not the supply available throughout the entire marketplace. New biobased project developers must be aware that existing forest products companies are the most reliable buyers in the wood fiber supply chain; pulp and paper mills alone are part of a $10 billion industry that receives 9.5 million truckloads of logs and chips each year. Suppliers tend to give precedence to these established and reliable buyers even as new opportunities emerge.

Accepting “free land” from economic development committees. If there is no such thing as a free lunch, there is most certainly no such thing as free land. Economic development committees have a vested interest in attracting new business to their regions. However, committee members are simply not qualified to offer unbiased assessments of the wood basin, infrastructure, supply and demand, and many other factors that contribute to the success or failure of a wood-consuming manufacturing facility. Ultimately, the cost of factors such as low inventory and high competition from other facilities in the procurement zone could significantly outweigh the money saved on a land deal.

Equating the number of trees with the availability of wood fiber. A heavily forested area can create the illusion that a region enjoys ample feedstock supply. However, it is important to realize that not all visible trees are available for harvest. Questions about who owns the trees or whether the trees are in harvestable areas must be answered to accurately assess the available wood fiber supply. The age class and species density of the forest must also be considered when assessing supply over a 20-year period.

Assuming wood costs will rise or fall based on the historical trend line. The cost of wood depends on demand and the age classes of trees available to meet that demand. For example, stumpage prices can temporarily spike when new demand enters the market and pressures current forest resources. Pulp and paper mills, OSB mills, bioenergy and biochemical manufacturers compete for the wood-derived feedstock available in a supply region. The higher profit margins that some facilities enjoy compared to other facilities allow them to absorb higher feedstock costs and still remain profitable for sustained periods of time. Savvy biobased project developers must cultivate a strong understanding of market competitors and establish some elasticity in their supply chains to allow for price fluctuations.

“Ballparking” feedstock prices without a dependable forecast. To produce an accurate forecast, the starting price (weighted average market price at a precise moment in time) should be based on the highest-quality transactional data available. By starting the process with a specific price based on the actual market, the forecast will deliver a greater level of accuracy. Cost curves that are based on actual market data will incorporate the true quantity and price of delivered loads of wood fiber within a unique supply basin. Combining the cost curves of all facilities within a supply region yields the market supply curve, which results in a supply curve that accurately reflects the sum of current harvests and excess inventory.

Project developers who know with a high degree of confidence what they will pay for wood supply over the next 24, 36 or 48 months can better optimize wood procurement—both volume and price—manage inventory more effectively, and align facility feedstock and output with raw material price trends.

Preconditions for Feedstock Efficiencies

Because supply agreements cannot regulate the delivered volume of feedstock, the onus is on project developers to understand and manage the interplay of factors affecting feedstock availability and cost within individual supply basins. No two supply basins are alike, which is why the U.S. South is the current focal point of wood pellet production while other regions are less so. As noted above, bioenergy project success will chiefly be determined by whether a company builds into its business plans—from the outset—a thorough understanding of the specific supply basin in which it will be operating. Essential guidelines and preconditions include the following.

Right-size the plant to the supply basin. There are two options here: Choose the size of the facility, then find a supply basin that will support the facility, or find a supply basin and then right-size the plant to the available supply in the area. In the case of the U.S. South, pellet capacity is increasing as new facilities continue to come online to take advantage of plentiful pine resources.

Design facilities with flexible receiving capacities. Design facilities that are large enough to weigh and unload the required amounts of feedstock. The facility should also have inventory capacity large enough to accommodate the normal market ebb and flow of material due to weather interruptions. As noted above, establishing supply chain elasticity is imperative in an evolving, competitive market.

Control for price risk. Price risk is a reality over the course of a 20-plus year project. However, proactive project developers can control price risk by indexing supply agreements to documented market prices. Just as companies manage the risk associated with variability in operational costs by indexing them to the producer price index, projects that manage feedstock price risk this way will be more bankable.

The global wood fiber supply chain is complex, and the economic cycles and seasonal patterns that govern supply and demand for wood fiber must be primary considerations. As the housing market recovers, pulp and paper demand increases and bioenergy markets continue to develop, competition for wood fiber will intensify in certain supply basins.

The single biggest factor determining the success of a wood bioenergy plant will arise from how well project developers understand the nature and characteristics of the forest resources and industries within its supply basin. The responsibility is on them to locate their projects in areas that ensure a sustainable and affordable feedstock supply, which will ultimately drive a successful project.

Author: Stan Parton

Manager, Bioenergy & Biochemical Practice

Forest2market Inc.

stan.parton@forest2market.com

www.forest2market.com

Advertisement

Advertisement

Advertisement

Advertisement

Upcoming Events